Budget 2023 | New Industry Tax Incentives for Solar

The latest Federal Budget was released this March, announcing consequential tax savings for businesses investing in clean energy generation and energy conservation projects. The Budget was favourably received by the Canadian renewables sector, who welcomed its dedicated support to attract the private capital required to drive clean economic growth and chart new pathways toward net-zero.

The newly introduced 30% tax credit is a great step forward to facilitate reduction of carbon footprint for businesses. Combining the tax credit with accelerated Capital Cost Allowance creates unprecedented savings for companies, says Quebec Solar President Bartek Wlodarczak.

Among the proposed measures are important tax incentives for businesses and corporations investing in photovoltaic solar panels, among other clean energy generation projects. Should your business or corporation have been on the fence about availing itself to the many advantages and benefits of switching to or adding solar energy generation, then this announcement may be what enables your business to make the jump. Contact Quebec Solar now for your personalized business quote.

Under Class 43.1, which covers solar panels, eligible equipment may be written off at 30% per year on a declining balance basis. Note that generally, equipment eligible for Class 43.1 but acquired after February 22, 2005, and before 2025 may be written off at 50% per year on a declining balance basis under Class 43.2. Also, as detailed in the 2018 Fall Economic Statement , businesses may benefit from an enhanced first-year allowance for clean energy investments, granted that the specified equipment was acquired after November 20, 2018, and becomes available for use before 2028. This enhanced first-year allowance allows for full expensing (100% deduction) of photovoltaic electrical generation equipment, for instance, with a phase-out for equipment that becomes available for use after this year (2023.)

Clean Technology Investment Tax Credit

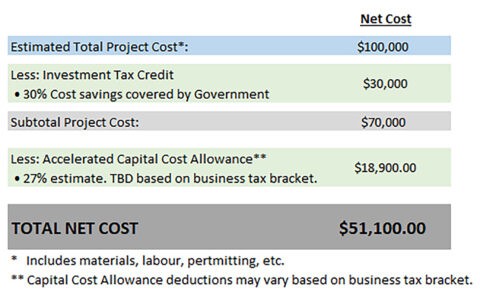

The Income Tax Act and Income Tax Regulations include vigorous measures to encourage Canadian businesses to make investments in qualifying clean energy generation equipment such as photovoltaic electrical generation equipment professionally designed and installed by Quebec Solar (see our gallery of projects). The 2023 Budget introduces a refundable 30% tax credit on capital cost of investments made by taxable entities in wind, photovoltaic solar and energy-storage technologies. This Credit will be available to all project spending starting March 28, 2023, though to 2034. A dollar-for-dollar credit against a company’s tax liability, investment tax credits effectively contribute to reducing the capital cost of an investment, making it more accessible, faster. Additionally, certain capital costs of systems that produce energy by using renewable energy sources, such as photovoltaic solar panels, are eligible for accelerated Capital Cost Allowance, or CCA, which refers to the federally sanctioned amount of amortisement expense a company is allowed to deduct from its income for tax purposes. Accelerated CCA allows businesses to write off a larger share of the costs of newly acquired depreciable capital assets in the year the investment is made or the asset becomes available for use. The example below shows how these incentives are combined to maximize your savings, which equates to a savings of 49%! Canadian Renewable and Conservation Expenses

Additionally to class 43.1 and 43.2 accelerated Capital Cost Allowance, if the majority of the tangible property in a project is eligible for inclusion in Class 43.1 or 43.2, certain intangible project start-up expenses (for example: feasibility studies and engineering and design work) may also be eligible as Canadian Renewable and Conservation Expenses (CRCE). These expenses may be deducted in full in the year incurred or carried forward indefinitely for use in future years. CRCE expenditures may also be transferred to investors using flow-through shares. In this case, the corporation may renounce the CRCE expenses that it has incurred to a person who acquires flow-through shares from the corporation. This allows shareholders to claim deductions as if they had incurred the expenditures directly. To qualify as CRCE, expenses must be incurred in relation to a project for which it is reasonable to expect that at least 50% of the capital costs of the project would be the capital costs of equipment described in Class 43.1 or 43.2. Given the eligibility criteria underlying each tax credit regime, it is certainly possible for a single piece of equipment or property to meet the criterial for multiple credits. Budget 2023 provides that, in such cases, only one credit may be claimed in respect of the relevant piece of property or equipment. Accordingly, it is recommended to carefully analyze which credit offers the greatest benefit in their circumstances. Projects must be assessed on an individual basis to determine whether particular costs qualify under Class 43.1 or 43.2 or as CRCE. The Canada Revenue Agency (CRA) is the final authority on tax matters and can provide, upon request, advance rulings on eligibility prior to incurring projects costs. Generally, principal assets used in energy generation and related equipment such as power transformers and control systems are typically eligible, while assets such as buildings and backup power supply equipment are not. As always, Quebec Solar offers step-by-step accompaniment to assist your business be as green and clean as it can be. Call us today for your personalized quote or more information on these latest clean technology measures. For more information: https://natural-resources.canada.ca/science-and-data/funding-partnerships/funding-opportunities/funding-grants-incentives/tax-savings-industry/5147Commercial Solar Quote Request Form

Companies, Institutions, Government Organizations we have worked with in the past: